Friday 5th June 2026

AI impact on Australian growth stocks is reshaping market assumptions

The AI impact on Australian growth stocks is beginning to show in valuations and earnings expectations. As artificial intelligence erodes competitive moats, investors are being forced to reassess which businesses can sustain advantage in a changing market.

Australian equities are entering a more challenging phase as artificial intelligence begins to chip away at the competitive advantages that have underpinned growth stocks over the past decade.

That is the message from ClearBridge Investments following a recent round of meetings with ASX‑listed companies, which suggests earnings risk is quietly building beneath the surface of what has otherwise been resilient corporate commentary. For investors, the AI impact on Australian growth stocks is no longer theoretical, it is beginning to show up in valuations and earnings expectations.

Earnings momentum is shifting as AI alters competitive dynamics

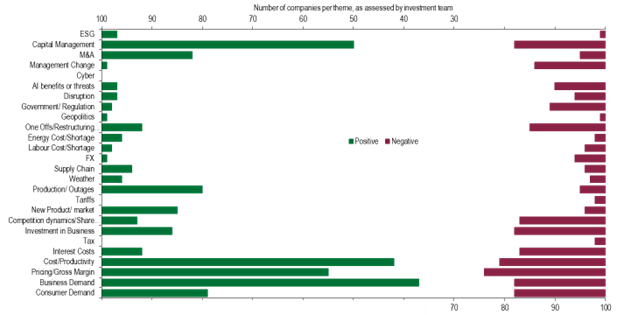

ClearBridge’s latest analysis of upgrades and downgrades across the S&P/ASX 200 points to a clear shift in what is driving earnings momentum. Traditional tailwinds such as consumer demand, business conditions, margin expansion and productivity remain broadly supportive. However, AI has emerged as a disruptive force, particularly for capital‑light, high‑growth businesses.

According to Reece Birtles, head of Australian equities at ClearBridge, recent company meetings revealed a growing disconnect between strong near‑term trading conditions and long‑term competitive risk.

“The standout in the data is how positive many of the traditional drivers have been. But the most impactful new theme is the threat of AI to software and content‑based companies.”

Notably, ClearBridge found little evidence that markets consistently reward companies claiming to deploy AI effectively. Instead, investor focus appears to be shifting toward moat erosion rather than productivity upside.

Economic moats are back in focus for investors

ClearBridge’s framework centres on the concept of the economic moat, including barriers to entry, cost position and resilience to technological disruption, to assess business quality.

For many established incumbents, scale, capital intensity, regulation and brand form the core of their competitive moat. Companies such as Telstra, the major supermarkets, Wesfarmers, Brambles, Medibank Private and shopping‑centre owners like Scentre Group exemplify this profile. These businesses typically have large physical footprints, with earnings closely tied to domestic economic growth rather than rapid market expansion.

In contrast, the past decade has seen strong investor support for capital‑light growth companies, especially in software, online marketplaces and digital services. Businesses such as Xero, Seek, CAR Group, REA Group and WiseTech Global have often been valued on the size of their addressable markets. High returns on equity have mattered more than the durability of their competitive moat.

AI is shortening competitive advantage periods

ClearBridge argues that the AI impact on Australian growth stocks fundamentally changes assumptions around pricing power, barriers to entry and long‑term earnings sustainability.

AI is lowering growth expectations, intensifying competition and compressing the period during which excess returns can be earned. A common theme from company meetings, Birtles notes, was deep uncertainty about how AI might reshape industries over the next decade.

“A recurring line from CEOs we met with was, ‘Who knows what AI is going to do to our business in 10 years?’”

By contrast, incumbents with significant physical assets may be better positioned to harness AI for near‑term cost efficiencies. Supermarkets, for example, can deploy AI to improve supply chains, pricing and labour productivity in ways that are tangible and quickly realised, unlike software businesses reliant on long‑term penetration of theoretical markets.

Valuation dispersion points to further adjustment

ClearBridge believes the market has already begun to reprice growth stocks, but the adjustment is far from complete. While de‑ratings have occurred, many growth companies remain expensive following extreme post‑Covid valuation expansion.

At the same time, ClearBridge’s proprietary valuation‑spread measure continues to sit near levels last seen during the tech bubble, the Global Financial Crisis and the Covid sell‑off.

Even after recent volatility and modest value outperformance, valuation dispersion within Australian equities remains unusually wide.

Defensive positioning reflects a changing market regime

Given these dynamics, ClearBridge’s higher‑conviction portfolios remain positioned defensively, with a bias toward lower‑beta stocks and caution toward cyclical exposures.

“In today’s market, it is the pro‑cyclical areas that appear most overvalued,” Birtles says.

As AI reshapes competition across industries, the message for investors is clear: in a market increasingly defined by technological disruption, the quality and resilience of the moat matters again.

Laurence Parker-Brown is head of content at The Inside Network and managing editor of The Inside Adviser and Investor Strategy News.